The case of FTX and the questionable merits of regulation

China's experience shows that competition works better than regulation

View from China with an Austrian School of Economics Perspective

Lots of articles are out over the weekend about the FTX collapse. FTX was a fairly new exchange launched in 2019 and effectively run by a group of children from the Bahamas. OK, maybe we’re being a bit unfair here – under 30 year olds.

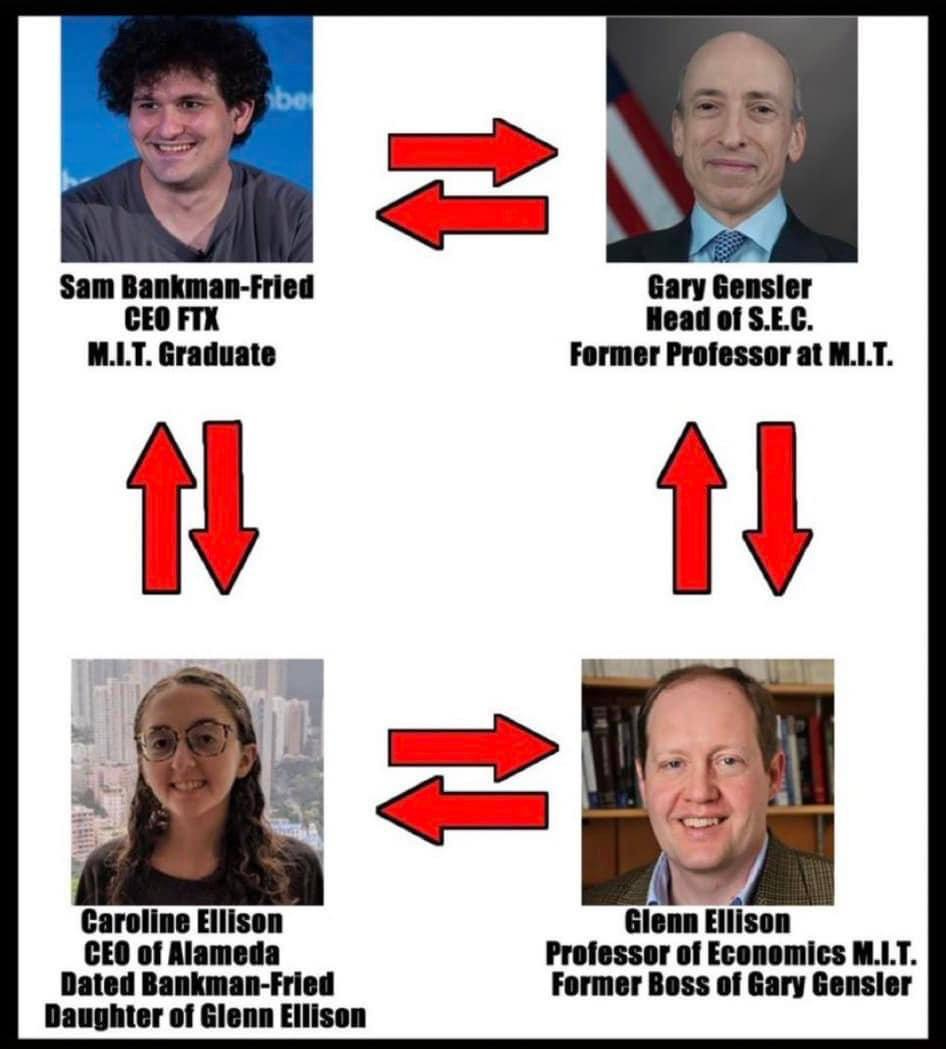

For those not in the loop, over the past week it emerged that now 30-year old ‘founder’ Sam Bankman-Fried (“SBF”) apparently embezzled around $10 billion from his exchange, diverting the funds to his so-called trading company Alameda. His very well connected 28-year old girlfriend Caroline Ellison was the CEO of Alameda, which is now broke.

We are writing in the past tense because as of this writing, FTX has declared bankruptcy and is apparently no longer operating. According to a number of reports, the remaining funds in their crypto wallets have all been cleaned out by ‘hackers’.

But let’s not forget he was doing it all for a good cause.

Both Sam and his girlfriend claim to adhere to the ideas of ‘effective altruism’ - often abbreviated as ‘EA’. According to Wikipedia, a key component of EA is so-called "cause prioritization". Cause prioritization is the idea that resources should be distributed to causes based on what will do the most good, irrespective of the identity of the beneficiary and the way in which they are helped. Where these resources are to come from and who is to decide on the most deserving causes does not seem to get much attention.

In 2017, Sam worked briefly at the Berkeley-based Centre for Effective Altruism as ‘Director of Development’. In her 2020 book Facing up to Scarcity, his mother Barbara describes her children as “take-no-prisoners utilitarians” (Acknowledgements, Page XV).

It is hard to escape the impression that Effective Altruism is a kind of a rehashed version of Marxism, where the acolytes decide on certain goals for the world and attempt to achieve these no matter what the cost (“take no prisoners”). In line with these lofty goals, the FTX exchange promised to devote 1% of the trading fees it collected to its ‘FTX Future Fund ’. According to an August 2021 article in ‘Inside Philanthropy’ it was focused on climate-related issues, e.g. investment in research and development of long-term carbon removal and reduction.

FTX’s most important ‘cause’ was however clearly the Democratic Party, allegedly giving over $10 million to the Biden campaign in 2020 plus $40 million for the 2022 elections.

Is more regulation the answer?

In all the excitement, it’s easy to lose perspective and forget that the cryptocurrency exchange business did not just get started in the past few years in the United States.

If we compare these events to what happened in China, there might be a few useful lessons on offer.

As we discussed in our intro piece we published 11 months ago, the current Chinese government has not been kind to its highly creative and dynamic cryptocurrency exchange sector. In 2017 it forced them all to leave the Chinese market, and last year finally managed to coerce the remaining top player Huobi into forcing its Chinese clients off the platform. To be sure, this was all done in a fairly civilized manner, without the seizure of servers or any clients losing money in the process, but one surely cannot claim that they enjoyed privileged treatment on the part of the state.

There was never any formal regulation of the exchanges in China, and the exchanges operated as they saw fit. Nor did this change after 2017. With the exception of BTC China, which was acquired by American investors, all the other major Chinese exchanges — OKCoin, Huobi and Binance — continue to operate today and remain for the most part unregulated. All of them have regulated subsidiaries in various jurisdictions, but their primary platforms continue to operate in cyberspace without any regulation.

And yet…. nothing significant ever happened. There were a few hacks here and there and some questionable behavior on their part, but there were no massive accounting frauds and/or collapses. Funds were carefully protected and where losses did occur were compensated for with reserves. At the very end of its existence, BTC China did fail to return some of the remaining customer balances, but the others never did, even when the Chinese government forced them to close the accounts of Chinese ID holders.

FTX on the other hand is a fine example of the exact opposite scenario. In the highly regulated American market it is both expensive and difficult to operate legally as a “money broker” in all 50 states. There are both state and federal regulations as well as licensing regimes which are very difficult to comply with. Many people have ended up in jail.

So how did the gang of children running FTX “succeed” where so many others did not? Why did it “grow” so quickly?

A thorough answer would doubtless be long, but the short answer is a very tight relationship with the regulatory and financial elite in the US – which are of course one and the same. Despite, or more likely, BECAUSE OF all these ‘regulations’ FTX was able to defraud its customers of billions of dollars. Most of the solid market players with long track records are excluded from the US marketplace; what IS available are a few companies with high level connections in government and Wall Street.

It doesn't have to be that way. There is a solution - it's called the free market.

The problem of moral hazard

If we think back to 2011 and the MF Global case, as the second largest donor to the Democratic Party in 2020, Sam has good reason to hope that he will get away with a slap on the wrist. In the case of MF Global, despite embezzling approximately $1.6 billion in customer funds, ex-Goldman Sachs CFO Jon Corzine did not spend a single day in jail. His only punishment was a $5 million fine.

Chinese exchanges by contrast never had any such luxury.

Sam pitched himself as the ‘most generous billionaire in the world’, proclaiming that he was “earning to give.” This is arguably not so hard when you are giving away your customer’s money and hoping you’ll be able to make it back on the next pump.

Though she did not use the term, Caroline Ellison put her finger on the core issue – moral hazard. She writes: “This blog endorses double-or-nothing coin flips and high leverage.” If bitcoin were at $200K today, maybe that would have worked out. But it’s not a good set of guiding principles for people entrusted with safekeeping billions of dollars in assets.

The Chinese hands-off approach seems to come out on top.

Unsurprisingly Sam was a big advocate for more crypto-related regulation from Washington - for his competitors of course. A classic case of regulatory capture.